Global Market Outlook: Stocks Gain on Fed lowering Interest Rates hopes; Asian Markets Show Mixed Performance – 5 Dec 2025

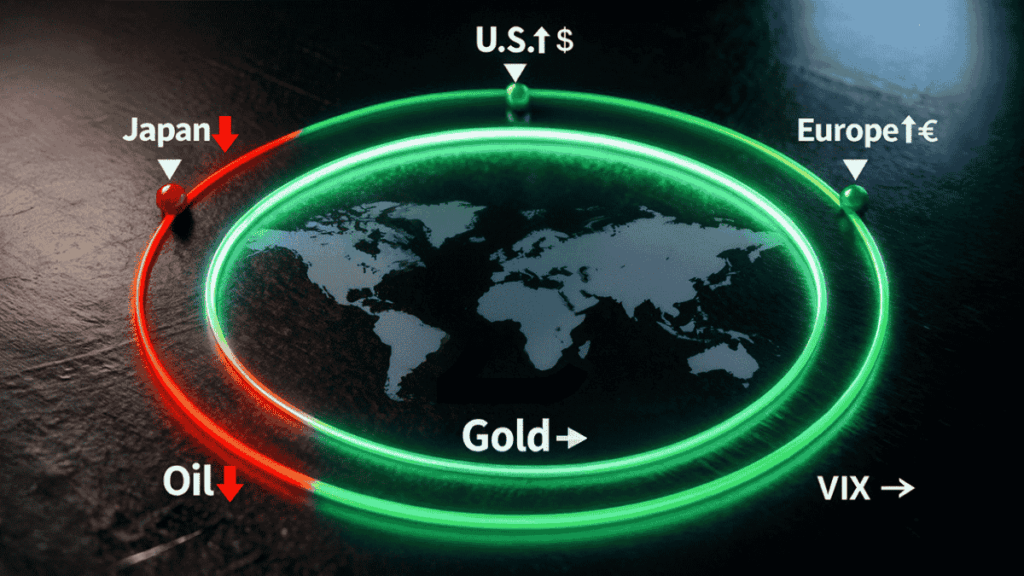

U.S. stock markets are almost at their highest levels ever because traders think the Fed will lower interest rates next week. European markets are slowly going up because industrial and car companies are doing well. In Asia, some markets are rising while others are falling, and Japan is going down. The U.S. dollar is also close to its lowest level in five weeks.

Market Note: Markets traded in recovery mode during the early 3 December session, supported by broad Asia-Pacific strength and improved risk appetite across equities and commodities. With no major U.S. data releases overnight, early price action was driven largely by regional flows and a calmer macro backdrop following the volatility earlier in the week.

Today’s Snapshot

- S&P 500 (4 Dec close): 6,857.12 (+0.1%).

- Nasdaq Composite (4 Dec close): 23,505.14 (+0.2%).

- Dow Jones Industrial Average (4 Dec close): 47,850.94 (–0.1%).

- STOXX Europe 600 (4 Dec close): 578.84 (+0.45%), led by industrials and automakers.

- FTSE 100 (4 Dec close): 9,710.87 (+0.2%), supported by hopes of a U.S. rate cut.

- Nikkei 225 (5 Dec, intraday): –1.3% as weak spending data and Bank of Japan hike fears weigh on Japanese stocks.

- MSCI Asia-Pacific ex-Japan (5 Dec, intraday): about +0.4%, supported by South Korea and parts of emerging Asia.

- CBOE VIX (4 Dec close): 15.78 (down from 16+ levels earlier in the week).

- Brent crude (5 Dec, intraday): ~$63.10/bbl (slightly lower on the day, roughly flat on the week).

- Spot gold (5 Dec, intraday): around $4,215–4,220/oz, broadly flat as higher yields offset a weaker dollar.

- US Dollar Index (DXY): ~99.0 (near a five-week low as markets price in a December Fed cut.

Global Markets

United States: In the United States, markets moved only a little. The S&P 500 went up by 0.1% to 6,857.12, and the Nasdaq rose 0.2% to 23,505.14. The Dow, however, slipped 0.1% to 47,850.94. The market stayed calm because investors are waiting for next week’s Federal Reserve meeting, where many expect a 0.25% interest-rate cut. This expectation is keeping most investors steady and not making big changes.

Europe: In Europe, stocks continued to rise. The STOXX Europe 600 moved up 0.45% to 578.84, helped by stronger industrial and auto companies. In the UK, the FTSE 100 increased by about 0.2% to 9,710.87. Even though some UK economic data was weak, investors focused on the global outlook and the possibility that a U.S. rate cut could support market confidence.

In the UK, the FTSE 100 added about 0.2% to 9,710.87. Investors looked through weak construction data and focused instead on the global picture and the chance of a U.S. rate cut supporting risk assets.

Asia: In Asia, the market picture was mixed. Japan’s Nikkei 225 fell around 1.3% after weak household-spending data and growing expectations of a possible rate hike. However, markets outside Japan were more positive. The MSCI Asia-Pacific ex-Japan index was up about 0.4%, South Korea’s KOSPI rose roughly 1.4%, and China and Hong Kong traded close to flat, showing a steady but careful tone across the region.

Asset-class highlights

Equities: Large-cap U.S. indices remain close to all-time highs, with the S&P 500 less than 1% below its record. Small caps, measured by the Russell 2000, rose 0.8% on Thursday, showing improved risk appetite in more cyclical names.

Currencies: The U.S. dollar stayed near a five-week low as markets strongly expect a Fed rate cut next week. The dollar index traded around 99.0. The euro was near $1.16, sterling around $1.33, and the yen around 155 per dollar. A weaker dollar supports risk sentiment and helps commodities and emerging-market currencies.

Oil: Brent crude traded near $63.10 per barrel, slightly lower on the day but roughly flat for the week. U.S. crude (WTI) was around $59.5 per barrel. Prices are supported by hopes of a Fed rate cut and tensions around U.S.–Venezuela relations, but gains are capped by concerns about future supply and demand.

Gold: Spot gold hovered around $4,215–4,220 per ounce, little changed on the day. A weaker dollar supports gold, but higher U.S. yields (and the wait for key inflation data) limit the upside. The metal is consolidating after strong gains in November.

Volatility & positioning

VIX at 15.78 (4 Dec): This is lower than the levels above 17 seen earlier in the week, which shows the market is calmer now. Investors are still taking some safety steps, but there is no sign of panic. Most traders are keeping their trades small and careful ahead of important events like the Fed meeting and U.S. inflation data, rather than reducing all their risk.

What traders are watching

- Federal Reserve meeting (next week): Markets almost fully expect a 0.25% rate cut. Traders are watching the Fed’s guidance very closely: if the Fed hints at more cuts in 2026, equities may get another lift; if the message sounds cautious, we could see a pullback in risk assets.

- U.S. inflation data (PCE index): The Fed’s preferred inflation measure is due soon. A soft reading would support the “cut and stay easy” story. A surprise jump could quickly change expectations and hit rate-sensitive sectors like tech and growth stocks.

- Bank of Japan and yen moves: The market now prices a high chance of a Bank of Japan rate hike in December. Any hint of a policy change can move the yen and Japanese equities sharply, and may also spill over into global risk appetite.

- Oil price drivers: Traders are tracking headlines around Russia-Ukraine, U.S.–Venezuela tensions, and OPEC+ supply signals. These factors can quickly move Brent and energy stocks, especially into year-end when liquidity is lower.

- European data and UK outlook: Confidence surveys and budget details from Europe and the UK will shape views on earnings for 2026. Sectors tied to global trade and autos are especially sensitive to any new growth signals.

Market Quote of the Day

“Calm markets do not mean safe markets. They just mean investors agree on the story—for now.”

Sources

- AP News – U.S. market closes (S&P 500, Dow, Nasdaq, Russell 2000).

- Reuters – Asia and global markets, Japan Nikkei, MSCI Asia-Pacific, oil and gold levels.

- TradingView – European equities, STOXX 600 and sector performance.

- Alliance News / Morningstar – FTSE 100 close and UK market summary.

- Reuters – FX moves, dollar index, euro, sterling, yen, Fed cut expectations.

- Reuters – Gold market updates: spot and futures prices, Fed expectations.

- Investing.com – CBOE VIX index, latest close (15.78) and recent history.

- Economic Times- Oil price summary (Brent and WTI, weekly gain narrative).

Yesterday’s market recap

Thursday, 4 Dec 2025 — U.S. stocks stayed near record highs with small moves: S&P 500 +0.1% to 6,857.12, Nasdaq +0.2% to 23,505.14, and Dow –0.1% to 47,850.94. European markets extended their winning streak, with the STOXX 600 up 0.45% and the FTSE 100 up 0.2%. In Asia, sentiment was mixed, and traders focused on the coming U.S. inflation data and the Fed meeting. The VIX fell to 15.78, Brent traded around $63 per barrel, and gold held near $4,200/oz as the dollar stayed close to a five-week low.

Link: Read our previous extended recap on: Global Market Outlook: Fed-Cut Buzz & Geo Risks Stir Markets – 4 dec 2025.

Kind regards,

Centrino Capital – Finance & Research Desk

www.centrinocapital.com

Disclaimer:

This report is provided for informational purposes only and does not constitute investment advice, financial guidance, or a solicitation to buy or sell any financial instruments. Market data and figures are subject to change without notice. Trading leveraged products carries a high level of risk and may not be suitable for all investors. Always ensure you understand the risks involved.

T&Cs apply. For full terms and conditions, please visit centrinocapital.com